NHS medicine spend

The UK has robust measures in place to ensure that medicines and vaccines are both clinically and cost-effective before they can be used in the NHS.

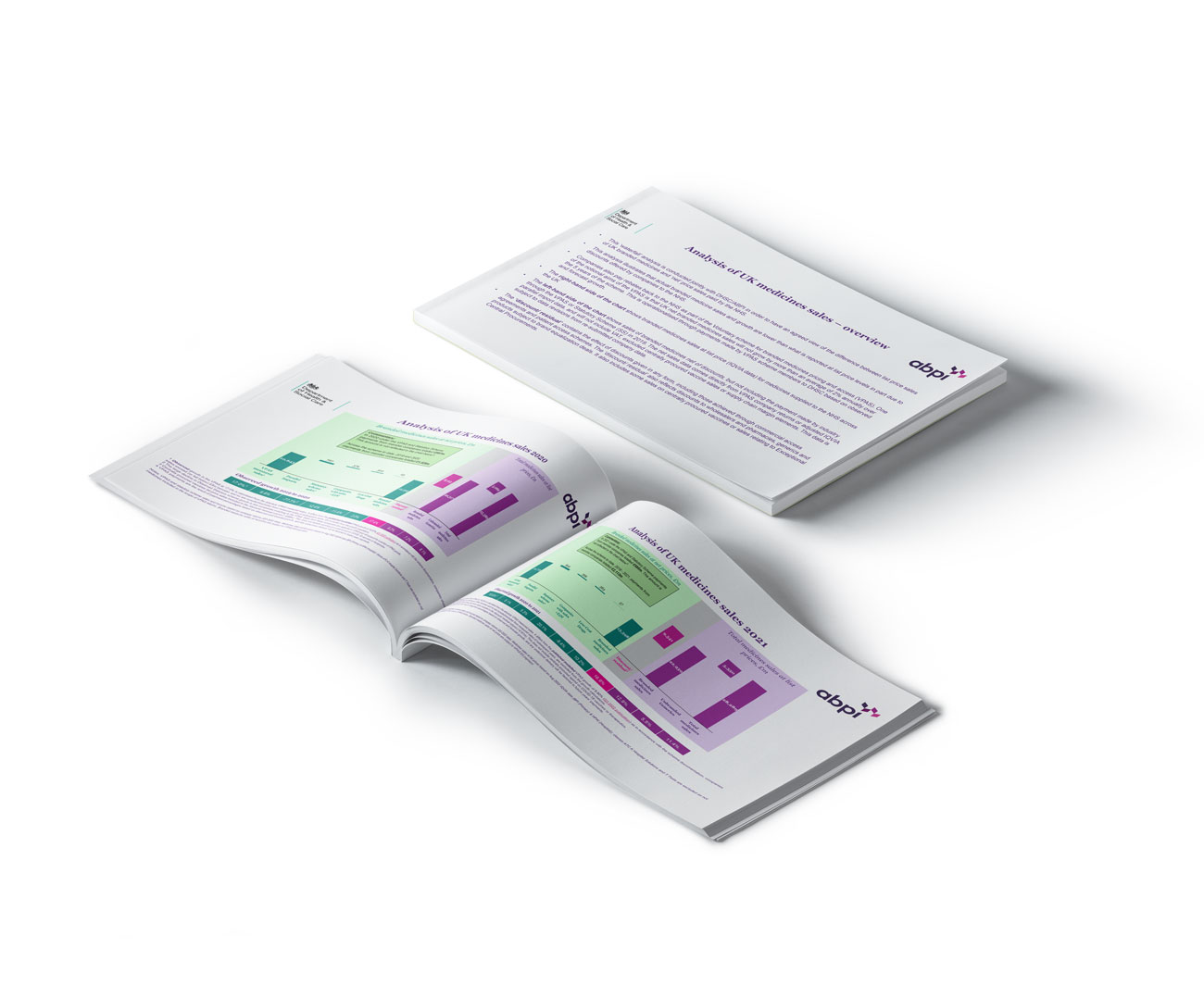

This ‘waterfall’ analysis is conducted jointly with DHSC/ABPI in order to have an agreed view of the difference between list price sales of UK branded medicines and ‘net’ price sales paid by the NHS.

Analysis of UK medicines sales in 2021

This analysis illustrates that actual branded medicine sales and growth are lower than what is reported at list price levels in part due to discounts offered by companies to the NHS.

Companies also pay rebates back to the NHS as part of the Voluntary scheme for branded medicines pricing and access (VPAS). One of the notional aims of the VPAS is that UK net branded medicines sales will not grow by more than an average of 2% annually over the 5 years of the scheme. This is operationalised through payments made by VPAS scheme members to DHSC based on observed and forecast growth.

The right-hand side of the chart shows branded medicines sales at list price (IQVIA data) for medicines supplied to the NHS across the UK.

The left-hand side of the chart shows sales of branded medicines net of discounts, but not including the payment made by industry through the VPAS or Statutory Scheme (SS) in 2019. The net sales data comes directly from VPAS company returns or adjusted IQVIA parallel import data, and will not include VAT, excluded centrally procured vaccine sales or supply chain margin elements. This data is subject to data revisions from re-submitted company data.

The ‘discount/ residual’ contains the effect of discounts given in any form, including those achieved through commercial access agreements and patient access schemes. The ‘discount/ residual’ also reflects discounts to wholesalers and pharmacies, generics and products subject to brand equalization deals. It also includes some sales on centrally procured vaccines or sales relating to Exceptional Central Procurements.

This analysis illustrates that actual branded medicine sales, and growth are significantly lower than what is reported at list price levels.

It must be noted that under the Voluntary Scheme, net branded medicines sales will not grow by more than an average of 2% annually over the 5 years of the scheme.

The voluntary scheme quarterly net sales and payment information is available online here.

The DHSC webpage, Waterfall Analysis of UK Medicines Sales also provides additional material, such as the data sources.

Last modified: 8 February 2023

Last reviewed: 8 February 2023

Last modified: 20 September 2023

Last reviewed: 20 September 2023